Steel-Manning the Tariffs

Even after engaging in the exercise, I think they're a fiasco

In 2003, right before the start of the Iraq War, I was sitting on the trading floor next to a trader who I worked with at the time, a Chinese national with whom I remember having very interesting conversations about the world. As President Bush delivered his final ultimatum, I remember the trader telling me that Bush had serious balls. This is a huge bet, he said. Big upside, huge downside, impossible to hedge and very hard to unwind—and no good way to estimate the odds. You’re going with your gut. Not the kind of trade he, personally, would be willing to put on his book. But he acknowledged nonetheless that it took real balls to roll those dice.

I’ve been thinking about that moment apropos of President Trump’s so-called “Liberation Day” announcement of massive tariffs on, well, everybody except Russia and North Korea, tariffs vastly in excess of what the financial markets anticipated. (I’m not the only person making the mental comparison; here’s John Judis yesterday on the same theme.) The move has the similar feeling of an enormous, massive roll of the dice. What are we rolling for, though?

The Iraq bet didn’t just require balls. It required a commitment to an idea, an assessment of the state of the world and America’s place in it and how those needed to change. 9-11 provided the pretext and the proof for action, but for those who believed in the idea the pre-attack status quo had been unacceptable for some time. America had allowed a specific problem—Islamist terrorism—to fester and grow to the point where it was an existential threat, and we now had to be willing to reorder the entire region to eliminate it at the source. We would bring democracy to Iraq, and thereby also change the political complexion of Iran, Egypt, Syria, Saudi Arabia, Pakistan—an entire global religion would be transformed through the judicious use of American arms. Even beyond the Islamic world, though, America had been allowing enemies and adversaries to grow in power and audacity, because we were unwilling to show the world just how powerful we really were. Taking Iraq wouldn’t just change the Middle East; it would clarify to countries from North Korea to Cuba that America was a global empire now, and they would have to reorder their politics accordingly.

That idea was nuts, in retrospect, and the wisest observers at the time saw that it was nuts in prospect. But they also saw something else: that without that animating fundamental idea, the whole war made no sense. Without the idea, all you were left with was an emotional impulse—we’ve got to do something more substantial after 9-11 than invading Afghanistan and hunting individual terrorists—bad risk analysis—can we really invade every country that might have a clandestine nuclear weapons program?—outright mendacity and political and bureaucratic inertia. The idea may have been nuts, but it was necessary.

What’s the animating idea behind Trump’s tariffs? Is it nuts? Is it even plausible that Trump and his team believe it?

That’s what I’m going to try to answer.

The animating idea behind Trump’s tariffs starts with a graph:

That’s a graph of America’s trade balance as a percentage of GDP over time. During the high-tariff era that lasted from the late 19th century through World War II, America ran a persistent trade surplus, sometimes an enormous one. This is also the period when the United States became the global manufacturing leader, and when Britain, the dominant global power, became increasingly indebted to the United States as it paid for two massive world wars along with the maintenance of an ultimately unprofitable empire. The United States, with a continental empire, was not greatly dependent on foreign trade for prosperity, but its approach to foreign trade was oriented largely around protecting American producers.

At the end of World War II, the United States was the overwhelmingly dominant economic power on the planet, and in that context established the Bretton Woods system of managed exchange rates between major currencies anchored by a dollar convertible to gold. The United States encouraged the development of allied economies and the outflow of dollars through programs like the Marshall Plan. As allied economies recovered, pressure on fixed exchange rates became a serious problem. Already by the late 1950s, the system was showing signs of strain, but the fiscal deficits and incipient inflation of the Johnson years made the existing arrangements untenable, and in 1971 the Nixon administration ended the system of fixed exchange rates and allowed the price of gold to float.

Since then, the United States has run persistent and large fiscal and trade deficits. We are able to run these deficits because the dollar is the global reserve currency, which means there is persistently more demand for dollar-denominated assets than assets denominated in other currencies, and that demand can only be met by creating dollar-denominated assets, namely: debt. This results in American interests rates being lower, and the dollar more highly-valued, than the economic fundamentals would otherwise dictate, which in turn is a boon to American consumers and to the federal government. But it has also been a persistent drag on American exporters.

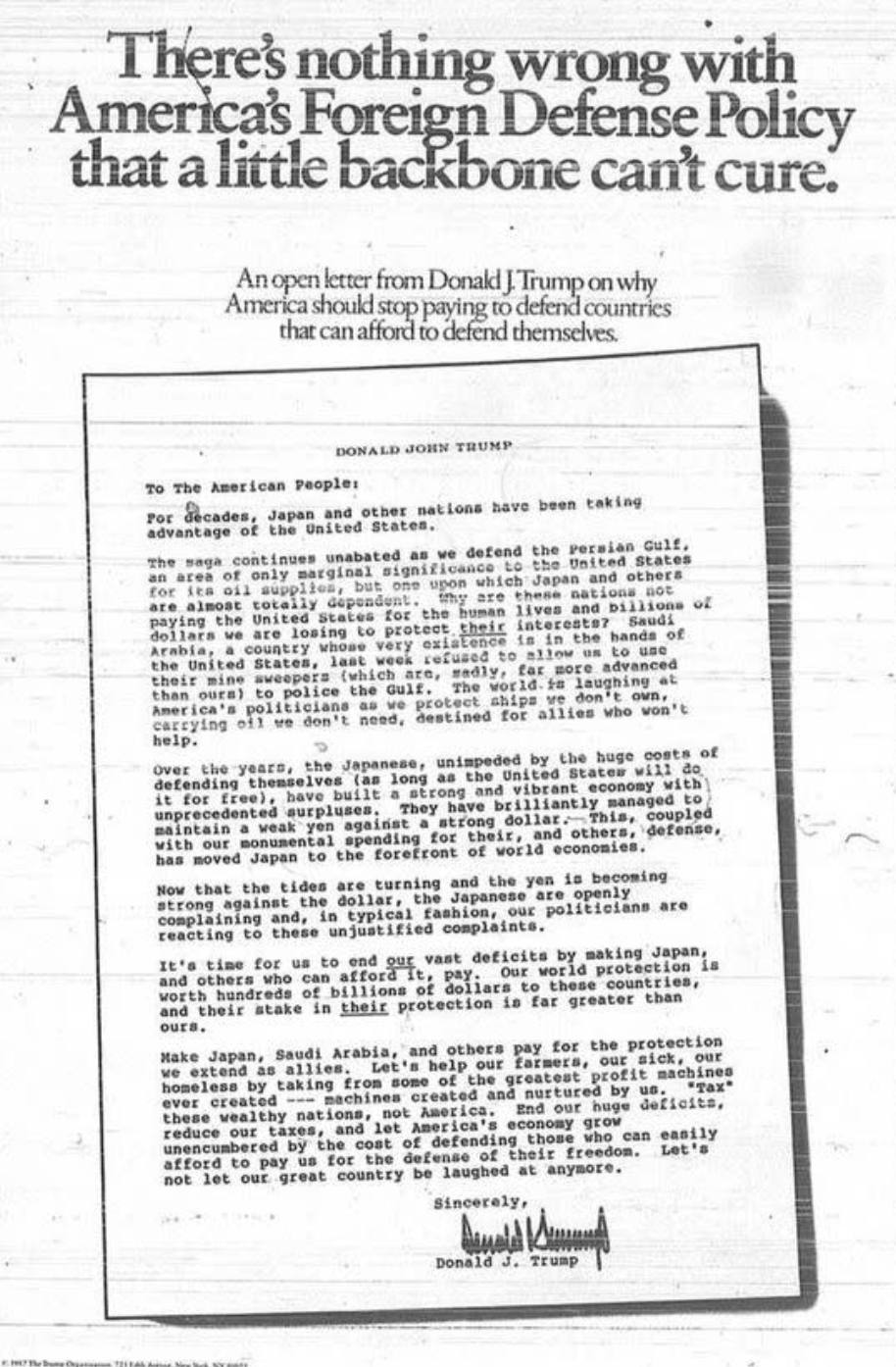

This was the story circa 1987, when Donald Trump took out his famous ad calling for America to impose tariffs and demand tribute from our allies:

The world has changed a lot since 1987—but the relevant changes went through two distinct phases. In the first phase, the Soviet Union collapsed, the United States got its fiscal house in order and experienced a surge of higher productivity, and Japan suffered through the first of its lost decades. By the year 2000, America’s percentage of global manufacturing output had been rising for a dozen years and was higher than it was in 1987—and nearly as high as it was on the eve of the collapse of Bretton Woods. America still ran a trade deficit, but it was hard to argue that it was an important drag on America’s international competitiveness.

In the second phase, though, America’s budget deficit has ballooned completely out of control, while the rise of China has completely transformed the shape of global trade and manufacturing. Both were plausibly made possible by America’s unique position as the global reserve currency, which allowed China for decades to recycle its massive trade surpluses by purchasing U.S. Treasuries, allowing America to grow in wealth even as it lost productive capacity. (I wrote about this in “The Greenspan Put Was Really a China Put.”) America is now a distant second to China in terms of the percentage of global manufacturing output, and can no longer claim to be consistently more technologically advanced. But we don’t just run a persistent trade deficit with China—we run one with much of the world, including with countries that run net trade deficits, while China runs persistent trade surpluses. In 2024, the United States ran a $235.6 billion trade deficit with the European Union, a $227.7 billion trade deficit with the states of the Association of Southeast Asian Nations, and a $171.9 billion trade deficit with Mexico; meanwhile, China ran a $247.2 billion trade surplus with the EU, a $190.7 trade surplus with ASEAN, and an $89 billion trade surplus with Mexico (in 2023; I couldn’t find 2024 numbers).

That’s the context for understanding the necessary idea behind Trump’s actions. Bretton Woods collapsed because as our allies recovered, the dollar needed to be revalued downward and currency rates needed to adjust dynamically going forward. The current system may not be in imminent danger of collapse, but persistent and large Chinese trade surpluses are reorienting the entire planet around China, and the United States is effectively propping up our allies’ continued competitiveness by allowing them to run trade surpluses with us even as they run trade deficits with China. If that situation persists for long enough, investors will cease to believe that America can pay back its massive debts. There will be a catastrophic collapse in confidence in the dollar, hyperinflation, and while China will also suffer, post-crash we’ll have a completely Chinese-dominated world economy.

I don’t think that’s a crazy thing to worry about. I worry about it myself—and I don’t disagree that jawboning China to rethink its economic model hasn’t worked, nor has pointing to the catastrophic trajectory of American debt made tackling it a political winner. So how are Trump’s tariffs supposed to prevent catastrophe?

The idea seems to be: force the collapse early and on America’s terms so as to forestall the most extreme outcomes. By raising enormous tariffs unilaterally not only on China but on our allies, the United States will make the continuation of the current trade regime impossible, provoking a sharp economic contraction and raising the specter of something even worse. Part of that “something worse” is a possible dollar collapse; America’s fiscal deficit is, after all, still underwritten by other countries’ willingness to buy our debt, which they do with dollars they receive from the goods and services they sell us. But we’re triggering it while we’re still enormously powerful and before other countries are prepared—it’s on our terms, not theirs. Facing impending catastrophe, all the world’s major economies—including China, whose economic model depends on running a massive trade surplus—will have to come to the table and negotiate a new trade and monetary regime, one that will be more balanced in America’s favor.

The precise contours of this new regime are a bit fuzzy, and vary depending on whether you are reading this lengthy piece by Stephen Miran, currently head of the Council of Economic Advisors, or this much shorter piece by the left-wing Greek economist Yanis Varoufakis, or this tweet thread—which I actually think is the best of the bunch—by Samuel Hammond, chief economist at the Foundation for American Innovation. The more fanciful scenarios involve persistent surplus countries like Germany and China agreeing to buy perpetual bonds to finance American debt, and also investing trillions in American manufacturing. America would thus remain the lynch-pin of the currency and trading system but without any of the downsides of the existing arrangement. This idea doesn’t even make sense in theory. More radically, but also somewhat more plausibly, the dollar would cease to be the global reserve currency, and be replaced by something else agreed upon by the world’s major economic powers—perhaps a commodity-backed currency or basket thereof, or perhaps something taken entirely out of sovereign control. American interest rates would go up, forcing a significant fiscal retrenchment, and the dollar would be permanently devalued, all of which would hurt American consumers. But China would perforce abandon its mercantilist economic model, and America would become much more competitive. The transition would be about as popular as the stagflation of the 1970s, but maybe after a decade it would genuinely be morning in America again.

That, in any event, is the idea. Is it nuts? Probably. I can’t fathom why our allies, for example, would want to reorder the world’s economy to be even more favorable to the United States right after we blew it up in their faces. Why wouldn’t they negotiate with China on a new arrangement, and then present us with a fait accompli? Or perhaps there would be no new arrangement at all—perhaps we’d just trigger the catastrophe, and in the free-for-all that ensued every country would seek its own advantage without any coordination—another outcome that probably puts China in the catbird seat. I also don’t understand why, if our fiscal situation is such a disaster (which it kind of is), you’d make things worse by provoking a massive recession followed by de-dollarization that permanently elevates interest rates—unless the goal is really resetting the domestic distributional baseline first and foremost. In any event, this isn’t how Reagan dealt with the overvalued dollar, nor how Bush and Clinton dealt with exorbitant deficits.

But there’s another problem with my steel-manning, beyond the question of how crazy the whole idea is in the first place. I can understand, perhaps, why President Trump might have wanted to look really aggressive, why he might have wanted to shock the markets—and even his own advisors—with the severity of the tariffs he imposed. I get the whole “madman theory” that Trump seems to be fond of. But there’s a different between having someone believe you’re crazy and having them believe you’re an idiot.

The tariffs President Trump slapped on the world on “Liberation Day” were calculated in an absolutely idiotic manner. The initial claim was that they were based on how much each of our trading partners was “cheating” us, but in fact they were just based on a simpleminded ratio between the bilateral trade deficit and the total amount of imports. The assumption seems to be that any bilateral trade deficit is caused by cheating—which is completely absurd. If America bought auto parts from Mexico and sold autos to Brazil while Brazil sold airplanes to Mexico, such that our triangular trade was perfectly balanced but we had a trade deficit with Mexico and a trade surplus with Brazil, this scheme would punish Mexico for cheating. (Moreover, according to the scheme’s “logic,” I suppose we should impose negative tariffs on Brazil because we’re running a surplus with them.)

More laughably, we imposed tariffs on islands inhabited only by penguins. Whatever idea may have been behind such moves, they make America look ridiculous. Dangerous, yes, but not in a “we’d better give them what they want” kind of way; more in a “we’d better take away their car keys” kind of way. If the goal is actually a “Mar-a-Lago Accord” to reset the global trade and currency system, you’d want the other powers coming to the summit to be competing with each other to win our favor. Faced with our obvious lack of seriousness, they’re more likely to coordinate with each other to stage an intervention.

I have an explanation for the dumb moves that you describe. Which, I also elaborate more on in my own writings :)

But anyways, the blanket 10% is not nuanced at all but that is the point. To get the point across, and to not spend time quibbling over details, you make it dumber and less nuanced and more blunt. 10% is the baseline, we might go over the penguin islands later, but it also doesn't really matter either way.

Secondly, Trump has taken what amounts to a disparate impact approach to trade. It is akin to school busing or EEOC lawsuits against companies for racial discrimination. Prima facie fairness isn't enough. If there is a disparity, that means that there is discrimination, racial or trade.

Again, disparate impact is a blunt approach that steamrolls nuance and attention to detail. But the point is to be blunt and impactful.

Excellent post! Draws torgether a lot of threads, thanks for digging up the Trump ad.

Regarding the Iraq analogy the key difference is character. Bush respected the architects of their brash and unrealistic plan, Cheney in particular. The brains were forming the policy.

Trump respects no one. The smarter people in his administration have a theory of sorts, but policy revolves around Trump's personal shortcomings (incuriousity, need for revenge, inability to conceive of a positive sum interaction, greed, etc.). Unlike Bush the dummy is generating the policy, Navarro/Bessent/Vance are reduced to supplying post-facto justifications.