Steering Into the Fiscal Crisis

In Republicans' minds, is it the early 1990s or the early 1980s?

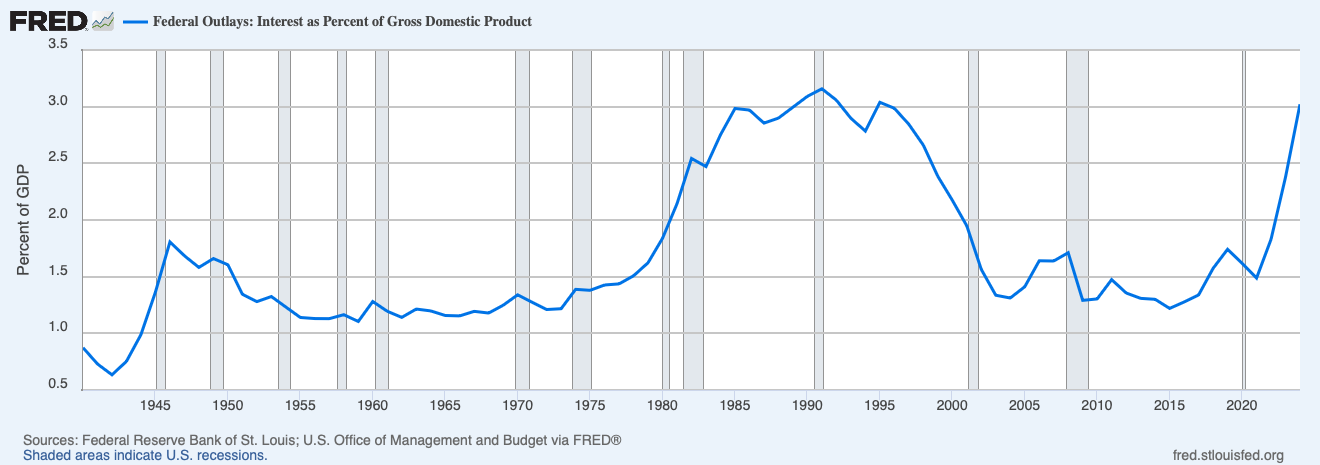

Federal interest payments as a percentage of GDP, from FRED.

Right before the 2024 election, I published a post arguing that whoever won, the two parties need to come together to deal with two major looming crises: our out-of-control budget and our overextended foreign policy. I argued that, in both cases, it was going to be very difficult to solve our problems in a partisan manner, and therefore, however difficult it was, we’d have to work together to solve them.

As it happened, Republicans won a trifecta, and since the election the Trump administration has been moving extremely swiftly on both fronts. On foreign policy, the administration’s extremely dramatic moves have already shattered the post Cold War security architecture. Europe is waking up to a world without the American security umbrella, Canada and Mexico grimly contemplate a world where America’s relationship to them is overtly coercive, and Russia and China have to consider whether they should seek to aggressively expand their power and influence, including through the use of force, or whether the real opportunity is to achieve a new modus vivendi with America and its erstwhile allies on much more favorable terms without the need for explicit aggression. But whatever happens, the status quo ante is no loner an option. The next American president, of whichever party, will have to maneuver in the world Trump created. It remains to be seen how catastrophic the results of Trump’s radical moves will be—or whether they might even turn out more positively than I currently imagine—but my assumption that we had to work in a bipartisan fashion seems likely to be proven false.

The budget looks like a completely different story.

DOGE is rampaging through the federal government, but its efforts to decimate the federal workforce have had no effect so far on government spending—as one would expect given that bureaucratic head count is a very small percentage of federal spending, that indiscriminate firing often leads to more short-term costs, and that for a while at least we’re still paying these people not to work. Maybe we’ll start to see savings if Congress actually does cancel some programs, but even then the amount of money involved is not consequential in the larger budget context. Trump’s major legislative initiative, meanwhile, is to extend the tax cuts from his first term which are set to expire. If enacted, this would massively expand the federal deficit at a time when it is already out of control. Whatever gimmicks Congress comes up with to let them do this while making it look like they haven’t done it, the bond market isn’t going to be fooled, so the ballooning deficit will also lead to inexorably higher interest rates and a large increase in the percentage of the budget going to debt service, a vicious cycle that makes the budgetary math harder to solve every year it continues.

These are very bad moves—but they also aren’t really a change of course. This is what American policymaking has looked like in the 21st century. The Bush administration passed a huge tax cut and also increased both domestic and military spending. The Obama administration arguably didn’t borrow enough enough given prevailing near-depression-level economic conditions, but it nonetheless did increase the debt substantially, both by extending some of those tax cuts and by increasing spending. The first Trump administration passed another huge tax cut and also increased spending, both before Covid and to an unprecedented degree during Covid. Then the Biden administration, in the face of the first substantial inflation since the 1980s, raised spending still further, and never seriously considered meaningful tax hikes. In other words, while in foreign policy Trump’s actions do constitute a major change of course, his administration’s budgetary proposals amount to accelerating even faster down the disastrous road that we are already on.

Which, actually, may be the plan.

A lot of observers, including myself, have compared our situation to that of the early 1990s, when we’d finally piled up debt to levels where the political system had to deal with it. And when it had to, the political system dealt with it. President George H. W. Bush and Democratic Senate Majority Leader George Mitchell agreed to a package of tax hikes and spending cuts, with the cuts focused on defense spending (the “peace dividend—over 60% of the net reduction in spending during the 1990s was in defense). Under President Bill Clinton the Democratic Congress passed additional tax hikes, and then lost the House, after which Clinton and Speaker Newt Gingrich enacted a variety of restraints on spending. The two parties didn’t just amicably agree to a balance of tax hikes and spending cuts, but between them they did come out in that place, and that’s basically what I assumed the bond market would force either a Harris or Trump administration to do.

We could run a similar play today, but it would be tougher both substantively and politically. First, and most important, the lift is bigger. In the early 1990s, during a recession, the federal deficit was around 4% to 4.5% of GDP. Today, during an economic boom (which may be ending), the deficit is over 6% of GDP—both because spending levels are higher and because tax receipts are lower. Second, the relatively low-hanging fruit isn’t there. We could cut defense drastically, but not without an even more substantial foreign policy retreat than we are already engaged in—and we’d have to cut far more deeply percentage-wise to achieve the same effect, because even though defense is still a very large percentage of the budget, as a percentage of GDP we spend about half today of what we did in 1990. Discretionary spending has also dropped as a percentage of the budget, and if anything we need to increase spending on all sorts of infrastructure for economic reasons. That leaves entitlements and taxes. Entitlements have ballooned as a percentage of the budget (largely but not solely due to the aging of the population), but Democrats define themselves by their defense of these programs, and Trump’s rebranding of Republicans as equally fervent defenders has a lot to do with his initial success (not to mention that a lot more Republican voters now avail themselves of Medicaid, SNAP benefits, etc.). Finally, the federal tax code has gotten more progressive since 1990, especially at the low end, and the Democratic Party has gotten more averse to broad-based taxation even as the Republican Party seems increasingly to believe that there should be no taxes on any kind of income or assets.

Given all of the foregoing, a responsible, balanced approach is going to be wildly unpopular with both parties’ bases as well as with the general public. For example, instead of extending Trump’s first-term tax cuts, the GOP could take the more balanced approach of simply letting current law stand and then tackling the debt by slashing Medicaid. Then Democrats would run against Republican Medicaid cuts and in favor of a wealth tax (which could in theory generate an enormous amount of revenue, but which probably wouldn’t work and might well be struck down as unconstitutional anyway), and likely win back the House at a minimum. That, in turn, would reinforce the existing dynamic against spending cuts and against broad-based taxation. Precisely because that response is available, it would be irrational for Democrats to agree to help the Republicans take the blame for an unpopular balanced approach to cutting the deficit in the first place.

Since Republicans know that too, the rational move for them is to steer the country into an even more severe fiscal crisis in a way that sets the policy baseline in the most favorable place for them. To put it another way, maybe we’re not in the early 1990s but in the early 1980s.

Take a look at that graph at the top. In 1980, in peacetime, America’s debt service costs passed their prior peak in 1946, just after World War II. The responsible thing to do would have been to hike taxes and cut spending and get the budget under control. As we all know, though, that’s not what the Republicans did.

The Kemp-Roth tax cut of 1981 was truly gargantuan, and between it and the 1982 recession the deficit spiraled completely out of control. But that bill also reset the policy baseline. The tax increases passed in 1982, 1983 and 1984 were all quite significant—the 1982 increase was bigger than either the 1990 or 1993 tax hikes. They didn’t completely offset the 1981 tax cuts, nor did they stop the cost of debt service from continuing to rise even as interest rates started to fall. What they did, and were intended to do, was lock in the 1981 policy framework. Payroll taxes went up, the retirement age went up, loopholes of various kinds were closed—but the headline rates didn’t go up. Indeed, they dropped further with the bipartisan 1986 tax reform.

If you went to Democrats today and said “we’ve got a big deficit problem, so we want to cut Medicaid, cut Social Security by changing the way COLAs are calculated, and eliminate the mortgage interest deduction” they would say “no,” run against you for doing or even wanting to do those things, and win. But if you enact an enormous tax cut that makes the deficit situation worse—and also cut Medicaid, cut Social Security, eliminate the mortgage interest deduction and who knows what else—then in 2027 if the Democrats take the House they’ll be negotiating, in the context of a still-enormous deficit, to trade some other concession to try to reverse at least some of that. Making the crisis worse by doing what they want to do anyway would thus give the Republicans leverage over the long-term shape of both taxes and spending.

Or consider the most dramatic and efficient way on the tax side to fix our budget problem: passing a value-added tax. A VAT is one of the most economically-efficient revenue-raisers out there; that’s why nearly every OECD country gets a significant percentage of revenue from one. Indeed, the gap between American tax receipts and the OECD average can be almost entirely accounted for by the fact that we don’t have a VAT. But passing a VAT would be political suicide: it’s incredibly broad-based and takes money out of people’s pockets in a very visible way at a time of acute concern about the cost of living. Trump’s tariffs—which have a similar effect but are both less economically efficient and more instinctively popular (because they appear to be levied on foreigners)—are already generating a backlash. I could only see a VAT being passed in response to a truly terrible crisis. So maybe this government will engineer that crisis—and then solve it by agreeing to a regressive tax hike that now would have Democrats’ fingerprints on it as well.

I don’t know that that’s the plan. I doubt that there is a plan. But whatever President Trump thinks, there are people on his team—and veterans in Congress—who can read a chart and see how bad things are, and who understand that in making the TCJA permanent they’re making a deep hole much deeper. So it’s easier for me to believe that they want to make our fiscal situation worse in order to change not only the shape of taxes and spending but the political dynamics of debates about that shape, than that they actually believe DOGE is going to right the federal budget by shuttering USAID.

The strategy may fail—playing chicken is a great way to get yourself killed. But there is a logic to it.