Is There a Simpson's Paradox Lurking In the Wage Growth Data?

Yet another round on the economy and how good it is

Today was an excellent day for economic news, with a surprisingly strong jobs report I think the two bits of conventional response—that this will boost President Biden’s political fortunes at least somewhat, and that it will also make it easier for the Fed to go slow with rate cuts—are both correct. We may not have a “better than Goldilocks” economy, but we could do way worse than leveling out and cruising (a better airplane-related metaphor than “soft landing”) right where we are now. So I give three pretty unequivocal cheers for the Biden-Powell macroeconomic policy.

Nonetheless, while reported consumer confidence is finally coming back into line with economic fundamentals, the question of why it diverged so dramatically remains something of a mystery. I took two stabs at the question before here and here. This is going to be a brief third entry, though at this point I’m less concerned to explain public opinion—that will be what it will be—and more concerned to make sure we understand the contours of the current recovery correctly for its own sake.

To that end, three recent Kevin Drum posts about the educational composition of the work force made me sit up sharply. Here’s the first, here’s the second and here’s the third. The first post lauds the surge in productivity since the start of the pandemic, pointing out that it’s normal for productivity to surge during recessions—the least-productive workers are the first to be laid off, and employers are especially determined to wring the most output per hour out of their remaining employees, and have more leverage to achieve that goal than they do in better times. But that surge is usually offset by a drop in productivity growth once the economy has recovered, employment is low, and the leverage goes the other way. This time, though, while there was a stall in productivity in 2022, productivity has surged again in 2023. Productivity just seems to have jumped to a higher level and stayed up. Why?

Well, Drum goes on to speculate, perhaps it’s because the composition of the labor force has changed fundamentally. Since 2020, the number of workers without a college degree has dropped 2%, while the number of workers with a college degree has surged 7%. Drum’s second post charts that change in the composition of the labor force since 2000, highlighting that it isn’t just driven by a change in the percentage of people with college degrees overall: since 2000, the share of the labor force with college degrees has outpaced the share of the overall population with college degrees by more than six percentage points, and you can see the same jump in 2000 that is only starting to close in 2023. By the end of 2023, 72% of college graduates were in the labor force, while only 57% of people with only high school diplomas were.

Some part—perhaps a very large part—of that longer-term change is likely due to age cohort effects. The cohort that has been retiring over any period in this century has a much lower percentage of college graduates than the cohort entering the labor force; that explains much of the long-term trend. And age cohort effects likely explain a significant part of the change since the start of the pandemic as well, because of accelerated retirements. Since the end of 2019, workforce participation by people over 55 has dropped by nearly 2% after being quite stable for the previous decade. But that shift in the composition of the workforce could all by itself affect other numbers like wage growth, or the differences in wage growth between college and non-college workers. Depending on the composition of the over-55 workers who dropped out of the workforce permanently since the pandemic, I could imagine it skewing wages up or down—or even in opposite directions for college grads and non-college grads.

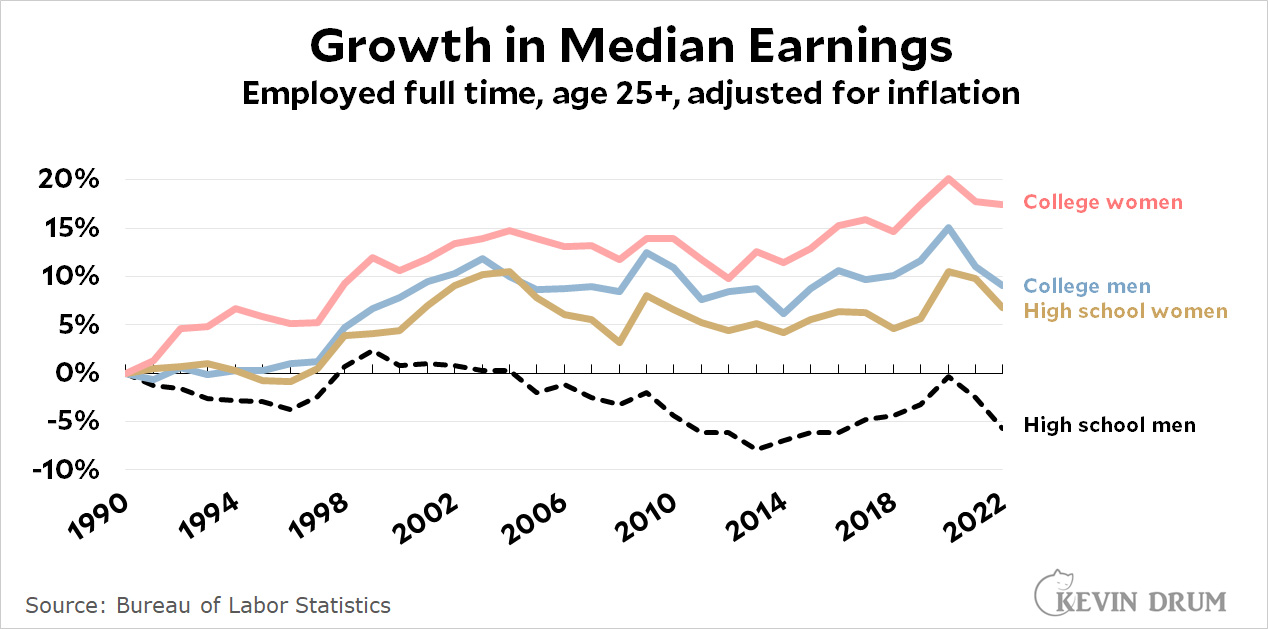

To the extent that this shift isn’t just age cohort effects, meanwhile, it suggests that one effect of the pandemic might have been a modest shift away from blue-collar work and towards white-collar and service work. Those are also long-term trends, but if there was a modest but meaningful jump during the pandemic, that might be relevant for explaining the disjunction between reports like this about how blue-collar wages significantly outpaced white-collar wages in 2022, and this chart which Drum cites in the third post I linked to above, which shows the relative wage performance (adjusted for inflation) of men and women, college grads and non-, since 1990. Unsurprisingly, men have lost ground relative to women (which is actually mostly women catching up to men), and high-school grads have lost ground relative to college grads. But, if I’m reading the chart right, both long-term trends manifested particularly strongly in 2021 and 2022. How can that be reconciled with the claim that inflation-adjusted median wages rose for non-college-grads? One possibility might be if there was a shift from men to women among non-college employees, reflective of a change in the job mix. And, indeed, women’s workforce participation dropped more than men’s during the pandemic, and yet recovered faster than men’s afterwards.

{kind=link}

I haven’t really dug into the data, so I may be completely off base in my speculation here. All I’m suggesting is that it’s always worth doing the digging. The macroeconomic data really is strong, and it’s real; I’m not questioning or undermining that. But when real people seem to disagree with the data, it’s always worth slicing the data differently to see whether it might reveal an explanation of the difference—not in order to “disprove” the aggregate data, but to reveal important complexities that aren’t immediately visible.

Perhaps we're seeing something with the "soft landing" that's simply never been observed before, since there's never really been a soft landing.

First, imagine the soft landing period as if it were a "recession-in-all-but-name". What would that look like? Well, inflation would surge. Obviously we can't have growth dip below zero, or it becomes a recession. And jobs would probably not go negative either. No, what we observed was that everyone just kind of muddled along until we got on the other side of it.

I think you and Drum are right that the productivity evidence is consistent with the overall turnover hypothesis. Sure, certain demographics might be doing better or worse, but the net impact is that with the economy doing "just so-so" during high inflation and at tight job market, we're really just churning a lot of low-productivity jobs into high-productivity ones. It's a game of musical chairs where the game-master keeps removing shitty old chairs and replacing them with brand-new ones. Not everyone gets the best chair -- the slow people still end up with worse chairs, many slow people quit and a lot of new fast people show up on the scene -- but everyone ends up with a chair they're more suited to than before, so net "enjoyment", AKA productivity, goes UP.

Other than that... I also kind of wonder if some of this is just the housing construction industry waking from its long slumber, leaner, meaner, and greener. A blunting of housing costs would register as a "productivity" bump.