Were the Modern Monetary "Theorists" Right After All?

They won't be happy with the political implications if so

Every now and again, someone comes along with an important insight that they cannot substantiate. We sometimes call this phenomenon being right for the wrong reason, and when we discover that someone has been right for the wrong reason, we tend to dismiss their original insight as mere luck. But it isn’t always just luck. Sometimes it’s a genuine if partial understanding of reality that has evaded people with more knowledge and experience of a particular subject.

I felt that way from the beginning about so-called Modern Monetary Theory (MMT). According to its adherents, our conventional understanding of economic policy is myopic in thinking of the federal budget as in any way constrained by limits on borrowing “capacity” and relying on the Federal Reserve to control inflation. We should not view fiscal and monetary policy as in any sense separate realms of policymaking; rather, anything the government does with money should be understood as entirely under its control, because money is a creation of the government by fiat. The implications include that the only reason for governments ever to collect taxes or to restrain spending is to limit inflation. MMT adherents therefore go on to argue for using fiscal policy primarily as a macroeconomic stabilizer, automatically raising taxes when inflation rises and massively expanding the scope of automatic spending increases during recessions.

The usual knock on MMT is entirely correct: what’s true isn’t new and what’s new isn’t true. More fundamentally, MMT is only generously called a “theory” because its adherents have never actually built a proper mathematical model of the economy that could be tested in any rigorous way. Noah Smith does an excellent job of knocking the stuffing out of the MMT folks and their credulous supporters here.

So why do I argue that the MMT folks were, in fact, at least partly right for the wrong reason? I’ll tell you.

What the MMT folks thought they were doing was making an argument for persistently high deficits. If the only reason deficits matter is because of inflation, and inflation is low (as it persistently was in the 1990s, 2000s and 2010s), then why worry at all about fiscal “prudence” when there are slack resources in the economy? But what they were really arguing, even if they didn’t always know it, was that fiscal policy was necessary to put those slack resources to work—that is to say, that the Federal Reserve could not engineer full employment on its own. They didn’t actually have mathematical tools to prove this, but they had a feeling that it was true, and their “theory” was the policy expression of that feeling.

I suspect that, in this, they were onto something. I can best explain what by contrasting their perspective with another, more respectable position within economics.

Market monetarists are basically the opposite of MMT folks: where the MMT folks think everything is ultimately fiscal policy, market monetarists think everything is ultimately monetary policy. They argued all through the Great Recession and its aftermath that the only reason the recovery was so slow and sputtering—indeed, the only reason the Great Recession happened in the first place—was that monetary policy was persistently too tight. If the Fed had consistently targeted nominal GDP rather than looking at inflation or commodity prices or other indicators to decide where to set interest rates, then it would not have tightened in 2007. Moreover, in 2008 and thereafter, it would have continued to expand its balance sheet without qualm until nominal income was restored to target. In the market monetarist view, the Fed is always capable of keeping nominal income on an even keel; all it needs to do is declare that this is what they will do, and the market’s expectations will rapidly shift, which in turn will change people’s decisions about spending and investing, and make that declaration a self-fulfilling prophecy.

Is that theory true? It’s hard to know for sure, because these kinds of all-encompassing theories can only properly be tested in a totalizing fashion. After all, one of the key postulates of market monetarism is that while the Fed can stabilize national income by fiat, it can do this only by declaring that, henceforth, this will always be its policy. Any doubt about policy consistency muddies the waters of expectations, which is the mechanism through which market monetarists believe the Fed ultimately acts.

But in the real world, we’ve had two recent tests of macroeconomic policy that shed light on the question of whether we “need” to use fiscal policy to stabilize the economy or whether the Fed can do it on its own. In the aftermath of the Great Recession, the Fed massively expanded its balance sheet, but fiscal policy quickly contracted—and we had a long, slow recovery with massive structural unemployment. By contrast, during the pandemic, the Fed even more massively expanded its balance sheet, but fiscal policy was also unprecedentedly expansionist—and we had an extraordinarily quick and complete recovery and an outright drop in poverty. To a non-economist, that would suggest that maybe fiscal policy does have a necessary role to play in stabilizing the economy.

Now, that doesn’t mean the MMT folks are right, because they don’t have a useful explanation for why fiscal policy would be necessary, either in theory or in practice. One reason might be that the zero bound on interest rates poses more of a problem for the Fed’s ability to reflate than market monetarists think it does. (I associate myself with that view.) Another reason might be that fiscal and monetary policy levers have meaningfully different distributional effects that are relevant to economy-wide aggregates like inflation. (I associate myself with this view as well, though more tentatively.) We’re still a long way from practical advice to policymakers.

But if that insight is correct, it’s worth asking whether it is symmetrical. That is to say: it’s worth asking whether it has implications for our current situation, which is characterized by persistent inflation rather than persistent unemployment, and which has (so far) also proven resistant to control solely through monetary policy.

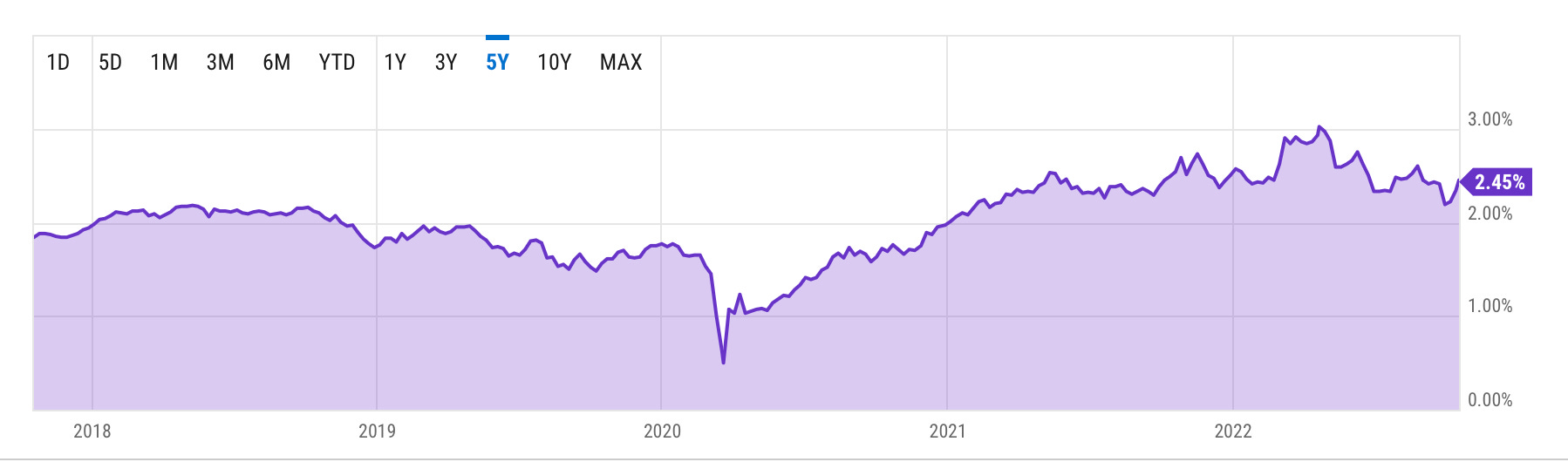

Of course, a market monetarist might object that the Fed still hasn’t been following their program; it hasn’t explicitly targeted national income and hasn’t raised rates as drastically as it might have to do to signal clearly to the markets that it intends to stabilize national income back on trend. (Which, I note, we got back to over the summer.) But the Fed has been signaling quite clearly that it intends to wrestle inflation to the ground, and, importantly, the market seems to believe they will succeed. Here, for example, is the 10yr TIPS inflation breakeven rate over time:

2.45% is high relative to the pre-pandemic norm of just under 2%, but not alarmingly so, and while the number has gotten more volatile it is trending down from its 2022 highs. If the Fed operates by shaping market expectations that become self-fulfilling prophecies, then it seems like they are doing a decent job.

Yet inflation remains stubbornly high. Why?

Matt Yglesias—like myself also not an economist—made the argument yesterday that what’s going on is that we’re still dealing with the long tail of the economic shifts that happened during the pandemic. Specifically, the combination of reduced household discretionary spending during the pandemic coupled with massive fiscal stimulus dramatically padded household savings. Now people are spending down that savings, and so long as they still feel that sense of “excess” savings, and so long as inflation remains positive (so that people expect future prices to be higher than current prices), they are going to continue to spend. That means demand will be too high relative to supply, which means that prices will continue to rise. The Fed, of course, is supposed to be able to dampen demand by flicking a switch—they’re supposed to convince people that inflation is going to come down which, when combined with the high rates of interest available on bonds, should induce people to shift from consumption to investment, which should produce that self-fulfilling prophecy. But it’s not happening, at least not enough and not yet. So Yglesias suggests that what we need (in addition to regulatory and other policy reforms to improve the supply side of the economy) is a strong dose of contractionary fiscal policy: cutting the deficit.

I don’t know whether Yglesias is right or not. What I do know is that by assuming the Fed can’t do its job all on its own—or can’t do it quickly and efficiently enough—he’s partaking of the same intuition that animated MMT from the beginning, this time on the inflationary side of the ledger. So it’s worth asking: if you did believe there was an essential role for fiscal policy in bringing inflation down, what would that role be?

Sadly, if what you’re trying to do is reduce excess demand in the economy, what you need to do is take money away from the people most inclined to spend it. That is to say: you either need to raise taxes on or cut benefits to middle-class people.

The reason for this is simple. The wealthier you are, the smaller the percentage of your income that you spend on consumption, and therefore the less likely you are to shift your overall spending in response to shifts in income. By contrast, most people have only a modest amount of savings, such that their discretionary spending can shift substantially in response to changes in their economic circumstances. This is precisely what Yglesias thinks is happening now: ordinary people have more savings than they are used to, and so they are spending it even though prices are rising and wages are not keeping pace. If you want to reverse that, you have to reverse it: take money away from people who are most inclined to spend it if they have it.

It should be obvious why nobody in the Democratic Party is advocating this: it’s politically toxic. Indeed, it’s so obviously politically toxic that Yglesias himself thinks the best political move for the Democrats to make right now in campaigning for the midterms is to highlight Republican plans to hold the debt ceiling hostage to force cuts in Social Security, Medicare and Medicaid, which he considers the most dangerous thing about the prospect of a Republican Congress:

Yglesias isn’t wrong that debt ceiling crises are incredibly destructive; that’s why we should get rid of the debt ceiling entirely (something the Democrats could easily do today if they wanted to). But from a purely macroeconomic perspective, cutting Social Security is precisely the kind of move that would reduce demand. And raising taxes on the non-rich—which Yglesias favors instead of cutting entitlements—is no less toxic than cutting entitlements.

This is the political conundrum in a nutshell. One reason we’ve delegated so much power to the relatively unaccountable Federal Reserve is that we want the economy to be stabilized successfully, which means operating in a technocratic fashion, not one liable to corruption by short-term political motives. (Over the longer term, we do want the Fed to be subject to democratic pressure to adhere to both parts of its dual mandate, which I would argue it has been.) If the Fed can do that job, then the legislature can focus on spending priorities and leave stabilizing the economy to the technocrats. But if the Fed can’t do that job on its own through its existing tools, and fiscal policy needs to lend a hand, then we have to do one of two things. Either the legislature needs to figure out how to do fiscal policy in a cooperative fashion even when they risk a political backlash, a profound challenge in our hyper-polarized era; or we need to delegate a chunk of fiscal policy to the technocrats (something Yglesias has suggested in the past on the spending side, though never on the tax side), and further reduce the accountability of our government to the electorate.

Or we need to live with periodic and painful bouts of inflation and/or recession, which I suspect is where we actually end up. The MMT folks didn’t discover a novel theory that allows us to have our cake and eat it too. Rather, in spite of themselves, they revealed the limits of a politics that sometimes has to not only take away the cake entirely, but make people give back what they’ve already had.

Speaking as an Australian, you might want to consider why Australian macroeconomic policy was so stable until the pandemic. The market monetarist analysis gives the best basis for understanding this.

https://www.econlib.org/lucky-to-stabilize-ngdp-not-inflation/