Inflationary Expectations

Inflationary Expectations

We shouldn't plan on low rates returning any time soon

Market yield on U.S. Treasury Securities at 10-Year Constant Maturity over the past 30 years, courtesy of the St. Louis Fed

Reactions by various friends to today’s inflation report suggest to me that people have had somewhat unrealistic expectations about what was going to happen with interest rates in the near term. Yes, the report was a disappointment—inflation has remained stubbornly higher than is desirable, and yes, that makes it less likely that the Federal Reserve will cut rates in the short term. But rates are not extraordinarily high now, and the reality is that rates at this level are entirely consistent with a healthy economy. Indeed, we shouldn’t want rates to get down to where they were in the wake of the financial crisis or during the worst of COVID—because they’ll only do that in the context of some new and similarly extreme crisis.

Take a look at the graph above, of 10-year Treasury yields over the past 30 years. The current market yield of 4.36% is roughly in line with where the 10-year rate was in the mid-2000s. It’s below where the 10-year rate was throughout the boom years of the 1990s. Could it come down from here in the absence of a recession? Sure—but it could also easily stabilize in this area, even if inflation settles down to more like 2%, so long as economic growth remains strong and there isn’t some exogenous factor (like massive and sustained buying by a rising foreign power) driving rates down.

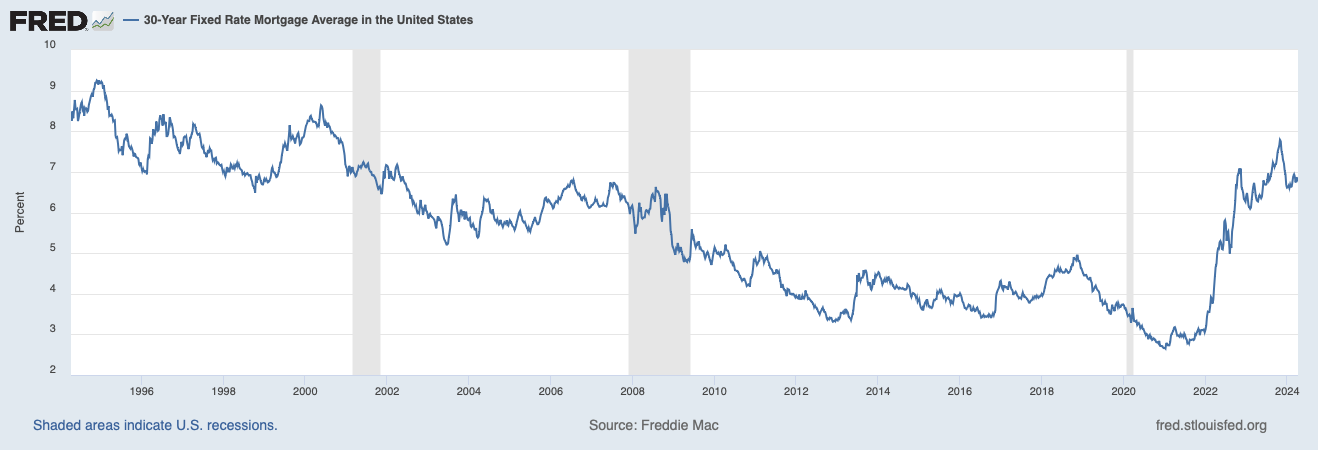

The comparison isn’t that different for 30-year mortgage rates:

The current rate of 6.82% is higher than the prevailing rates during the pre-crisis 2000s, but it’s below the prevailing rates of the late 1990s. I don’t think it’s unreasonable to hope that mortgage rates could come down a bit from here—to somewhere just below 6%, say. But the rates that prevailed in the 2010s were abnormally low, and we shouldn’t want them to return. The fact that they’d crept up to nearly 5% by late 2018 was a reflection of the strength of the economy, not something to lament.

Prevailing interest rate conditions, in other words, are normal. We’ve suffered a shock because rates backed up so quickly from incredibly low levels, but that’s also a reflection of how quickly the economy recovered from the exogenous shock of COVID. When you drive fast, you have to corner hard. And if we want a full-employment economy generally, we’re going to have to learn to live with significantly positive interest rates.

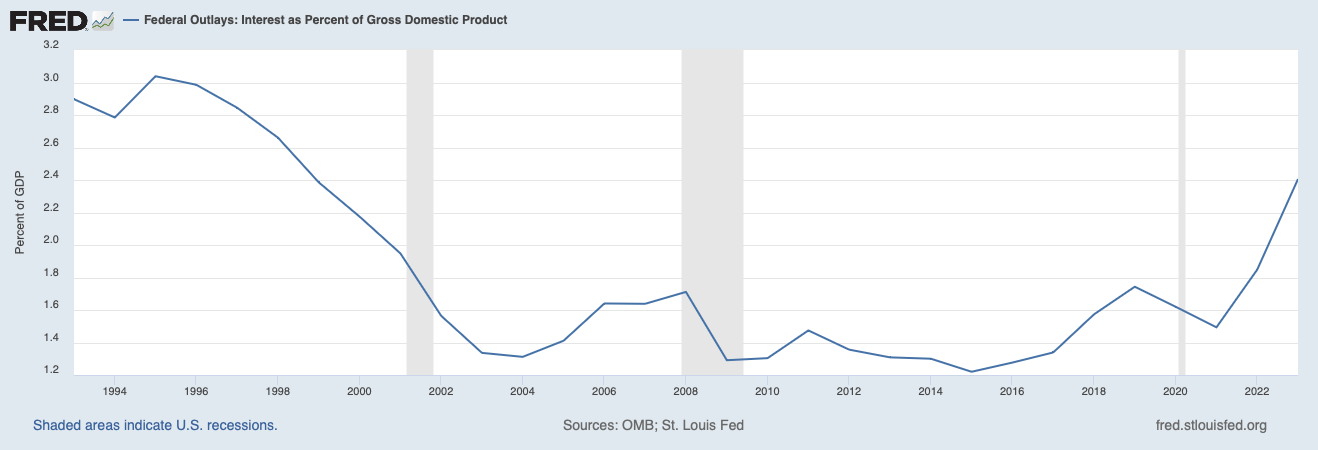

That means, among other things, that we’re going to have to learn to live with budgetary constraints again, something we haven’t had to think about since the 1990s. We’re currently running deficits of more than $1.5 trillion per year, even though we’re in an economic boom and defense spending is dropping toward a post-Cold War low as a percentage of GDP. The cost of interest on the federal debt has skyrocketed back to 1990s levels as well:

And yet, the deficit politics of the 1990s shows no sign of returning, at least not yet. The GOP remains focused on cutting taxes and the Democrats remain focused on boosting domestic spending. Josh Barro is probably right that it will take sustained pain from high interest rates to change voters’ perception of the importance of the deficit, and that it will take a change in voter perception to make politicians respond, because the politics of deficit reduction isn’t nearly as much fun as the politics of a free lunch. But that, in turn, means that we not only should expect interest rates to remain high, but that we should expect them to remain higher than they need to be given prevailing macroeconomic conditions.

That’s my big take-home from not only from today but from the last year.

If we imagined that our political system got interested in bringing the budget into some semblance of balance again, then we could get deeper into the weeds. Here’s a weed I’m particularly interested in: since the COVID-related supply-chain problems resolved, services inflation has stubbornly outpaced inflation in goods (which has been flat to negative lately). Wages are a bigger component of the cost of services than for goods (in general), and productivity growth has been tougher to achieve in the services sector than in manufacturing. All of that suggests to me that what the Fed is really waiting for is evidence of significant moderation in wage growth. As a political matter, that goal is surely a problem for the incumbent president—but it’s potentially an economic problem as well if we’re actually trying to run a full-employment economy. Can you do that for any length of time without wage growth starting to feed into services inflation in a significant way? I wonder.

Then again, once ChatGPT starts taking service workers’ jobs in a serious way, I suppose we can stop worrying about that problem.

I mean, you get to the core problem with the whole system at the end: high wages are high prices. It's pain in either direction. And in time Baumol's cost disease might really break capitalism.

Millman is talking about r*. What (real) interest rate [vectrof rates, but let's reify as the EFFR] is consistent with stable inflation? That is the standard definition or r* and that stable inflation rate is presumably the Fed's target in its FAIT (Flexible Average Inflation Target) framework.

Let me further stipulate that the FAIT rate should be a forward looking expected rate, not a backward looking arithmetic mean of the last n months AND that it be chosen as the target that maximizes real income. [There presumably are stable rates of inflation that are a) so low as to cause recession, b) too low to maximally facilitate the adjustment of relative prices in response to shocks, given that some prices (like real estate assets prices and leases) and wages do not adjust downwardly easily and c) too _high_ to maximally facilitate relative price adjustment and to formation of estimates of future relative prices.]

Now we can reformulate Millman's question as, what is r*? And the answer is that no one knows, although I'll go out on a limb to guess it is less than 5.25% and greater than near zero% I'll further guess that iti s grater than it was before COVID (whatever THAT was) because of the accumulation of more Federal debt and higher structural deficits.

See:

https://thomaslhutcheson.substack.com/p/arrrrr

https://thomaslhutcheson.substack.com/p/framework-for-monetary-policy-1

https://thomaslhutcheson.substack.com/p/framework-for-monetary-policy-2?r=8ylpe&utm_campaign=post&utm_medium=web